|

Because the nature of insurance is to secure versus the unguarded, you might just be covered if an unanticipated event happens. If it appears like you have a 50-50 opportunity of making the journey because of personal or business factors, it's most likely best to skip the journey completely. Travel insurance might compensate your purchases, however you might not wish to take that possibility. Although travel insurance supplies extra assurance, it's not always a smart purchase. These are some cases when you should not purchase travel insurance. If you're only driving five hours to check out far-off family members, you most likely do not require travel insurance. Losing money is never fun, but buying insurance for each small trip can cost more than the payout advantages when you finally submit a claim. If your only expenditures are plane tickets and hotel spaces, the carrier might reimburse or provide credit. Travel insurance coverage reimbursement just occurs if the travel company does not use reimbursement initially. Your automobile insurance supplier or travel charge card may currently provide rental car accident and theft protection. Getting travel insurance, mostly replicate protection suggests you're paying additional for minimal advantages. That's money you could be investing on your trip instead. Before booking travel insurance, inspect your present charge card and insurance advantages guide first. If you travel throughout typhoon season or a region's snowy season, you require to see how they treat inclement weather condition cancellations. Confirm their personal factor cancellation policies as well. http://paxtonpdjc873.trexgame.net/5-simple-techniques-for-what-does-home-insurance-cover You may be able to get an one-year credit to rebook your journey. To get the very best rates and coverage quantities, you need to buy travel insurance within 10 to 15 days of booking your travel bookings. After this date, you may need to pay a higher premium or choose a decreased policy. If your individual or work scenarios change after the travel scheduling date but before you buy a policy, you can likewise threaten your claim eligibility. If a typhoon (or another severe event) establishes and becomes public knowledge, you're probably far too late. The early bird gets the worm, especially when it pertains to travel insurance coverage. Travel insurance can be a financial blessing for large, non-refundable travel expenses. Whether they come from medical factors, severe weather condition, or wesley financial group reviews regional occasions, travel insurance can be worth its weight in gold. Even if it doesn't make good sense to purchase travel insurance coverage for this trip, acquaint yourself with policies and with your credit card travel advantages for future planning. Travel insurance coverage can lessen the significant financial risks of traveling: mishaps, illness, missed out on flights, canceled tours, lost baggage, theft, terrorism, travel-company insolvencies, emergency situation evacuation, and getting your body house if you pass away. Choosing whether to invest in travel insurance has actually always been a difficult decision, and naturally the coronavirus pandemic has actually made that option a lot more complicated. Here are some considerations to help you choose. Each traveler's prospective loss varies, depending upon how much of your journey is prepaid, the refundability of the air ticket you bought, your state of health, the worth of your luggage, where you're traveling, the financial health of your trip company and airline company, and what protection you currently have (through your medical insurance coverage, homeowners or occupants insurance coverage, and/or charge card). How What Is Florida Unemployment Insurance can Save You Time, Stress, and Money.

For some tourists, insurance coverage is a bargain; for others, it's not. What are the possibilities you'll need it? How ready are you to take dangers? Just how much is assurance worth to you? Take these factors to consider into account, comprehend your choices, and make an informed decision for your trip. The insurance coverage menu includes five main dishes: trip cancellation and disturbance, medical, evacuation, luggage, and flight insurance coverage. Supplemental policies can be added to cover particular concerns, such as identity theft or political evacuation. The numerous types are typically offered in some combination. As you weigh choices, think about the relative value to you of each type of coverage. Companies such as Travelex and Travel Guard deal thorough packages that act as your main coverage; they'll look after your expenses no matter what other insurance coverage you might have (for example, if you have medical insurance through your task). That implies they pay very first and do not ask questions about your other insurance. This can be a genuine plus if you wish to avoid out-of-pocket expenses. Insurance coverage prices can differ commonly, with most bundles costing between 5 and 12 percent of the total journey. Age is one of helping timeshare owners the greatest factors impacting the price: Rates increase considerably for every years over 50, while protection is generally economical and even complimentary for kids (under 18). How much is health insurance. ( If your journey gets canceled, don't anticipate insurance companies to reimburse policy premiums.) With medical protection, you might have the ability to set up to have costly healthcare facility or physician bills paid straight. In any case, if you have an issue, it's smart to call your insurance provider instantly to ask how to continue. Lots of significant insurance provider are accessible by phone 24 hours a day handy if you have issues in Europe. Also consider which categories may already be covered, to some degree, in other ways (What is whole life insurance). For instance, lots of credit cards include travel advantages (some degree of flight insurance coverage, car-rental coverage, and so on).

However, do not simply presume you're totally covered. Do some mindful research and be extremely clear on the limits of your policies. (For example, your stateside car insurance coverage more than likely will not cover you on European roads, and even credit-card protection is not always accepted by European rental companies.) Travel agents recommend that you get travel insurance coverage (since they get a commission when you purchase it, and since they can be held accountable for your losses if they do not describe insurance coverage choices to you). While travel representatives can offer you details and recommendations, they are not insurance coverage representatives constantly direct any specific questions to the insurance supplier. If you need to make a claim and encounter issues with a business that isn't accredited in your state, you don't have a case. When you're ready to call a travel insurance coverage company, make a note of any important concerns and have them all set. It's likewise wise to know ahead of time whether the policy is refundable or not and for the length of time. If you're insuring a tour or plan journey, likewise think about whether the policy covers any pre- or post-tour bookings, which can include different conditions. Some reservations are completely non-refundable. Examine to see which reservations you make (flight, hotel, transportation, tours, and so on) are covered by an insurance service provider if you require to cancel.

0 Comments

Insurance protection can be overwhelming, specifically for renters who do not understand that they need to secure their personal residential or commercial property. What is renters insurance coverage and why do you require it? Select ... Select . (How does insurance work).. INTRODUCTION WHAT'S COVERED METHODS TO CONSERVE FAQ. The average renters insurance cost in the U.S. is $168 each year, or about $14 each month, according to Nerd, Wallet's most current rate analysis. This quote is based upon a policy for a theoretical 30-year-old renter with $30,000 in personal effects coverage, $100,000 in liability coverage and a $500 deductible. While the across the country average is an useful standard, renters insurance coverage rates can vary considerably based on where you live and how much coverage you need. The location of your home is a major consider the Continue reading cost of your renters insurance coverage. Inspect just how much you can expect to pay for occupants insurance in your state listed below. If you live in the L.A. Basin or the Bay Area, you may end up handling a private insurer for your regular renters insurance coverage requires, and the CEA for supplemental earthquake protection. Before you confirm your policy, meticulously brochure your home's contents. You require to offer your insurance provider with a rough accounting of these contents anyway, but a more in-depth review is critical for your own records. Picture every product of worth that you own when your policy enters into result; to the extent possible, conserve the purchase invoices for each item as well. Do this for every huge purchase that you make after your policy goes into effect too. It sounds like overkill, but it's a reasonably little financial investment that can dramatically increase the possibility that your claim will be accepted if you experience a loss. Whereas property owners with active home mortgages are typically required to guarantee their homes, occupants with active leases face no such required. Not surprisingly, many tenants select to forgo renters insurance entirely - How much is gap insurance. Rather of taking out different or bundled renters insurance policies, they choose to construct up an emergency fund adequate to cover the cost of replacing their https://zenwriting.net/farela1xwt/selecting-a-higher-deductible-will-reduce-your-automobile-insurance-coverage apartment's contents. Is this strategy right for you? It depends. First, it is essential to remember that you can insulate yourself from certain types of risk specifically, liability for misfortunes that befall your guests, maintenance employees, and your structure's other occupants without guaranteeing all of your personal property. Although it might be tough for you to make the financial case for carrying content insurance instead of keeping an ample and well-managed emergency fund, it's more difficult to refute the advantages of fundamental liability coverage on your home. For starters, unguarded liability costs can rapidly spiral out of control if an injured guest requires to remain at the hospital overnight, you're easily taking a look at a five-figure medical costs. No matter how close your relationship with the hurt visitor, you shouldn't count on excellent graces to secure you from legal action. When it comes to liability, friendly visitors are the least of your worries. The smart Trick of How Much Does Homeowners Insurance Cost That Nobody is Discussing

You'll likewise be responsible to next-door neighbors who suffer residential or commercial property damage or injury as a result of a risk that originates within your apartment or condo. Even if you bring liability coverage for 15 or twenty years prior to incurring a claim, you'll probably pay far less than you would to settle a legal conflict over simply one over night healthcare facility stay for which you're discovered accountable specifically after accounting for legal charges. According to Insurance coverage. com, the national typical cost of an occupants insurance policy covering liability and personal residential or commercial property with a protection limitation of $100,000 and a $1,000 deductible is about $27 monthly, or $326 per year. In more "dangerous" locations where negative weather occasions prevail and criminal activity is greater, premiums can go beyond the average by 20% to 30%. When the alternative is an overall loss of furniture, clothing, and electronic devices with a collective worth of thousands or 10s of thousands of dollars, paying $326 annually or $3,260 over ten years prior to inflation looks like a no-brainer. Nevertheless, this heading figure is a bit misleading due to aspects such as your policy's deductible and coverage limitations. As you weigh the expenses and benefits of purchasing content coverage, it's helpful to break your options into these broad however distinct classifications:. Premiums on these policies are far greater than the nationwide averages priced quote above, however the tradeoff for this cost is assurance. If you seem like you require a top-tier policy, you most likely have some pricey or rare ownerships, and you may require to investigate riders or supplemental insurance to ensure that they're effectively covered. These policies come with low to moderate deductibles in between $300 and $500 and high coverage limits (more than $50,000) - What does renters insurance cover. They're especially useful for households or middle-class couples who prepare to lease for the long term; normal policyholders have great deals of stuff to safeguard, however may not be able or going to pay for top-tier coverage. With bigger deductibles in between $500 and $1,000 and lower coverage limitations (between $20,000 and $50,000), these policies are popular with more youthful, upwardly mobile renters who earn good incomes however have not yet collected great deals of high-value belongings or began families. They're helpful for protecting electronic devices, clothing, and other important however not extremely valuable products. Offered the size of the deductible and the potential for the cost of an overall loss to surpass the policy's protection limitation, your middle-of-the-road policy ought to be paired with an emergency situation fund. Similar to " devastating" health insurance policies, these instruments feature high deductibles of $1,000 or more and getting rid of a timeshare legally fairly low coverage limitations (less than $20,000).

Your gap insurance coverage works by assisting pay the difference between your lease or loan amount and insurance protection. For instance, say you total your automobile in a mishap. You still have actually $10,000 left on the loan, but your vehicle is worth just $4,000. In this case, your space insurance coverage can help cover the distinction between the 2, approximately your policy limitations. To purchase space insurance, you can call our representatives at $1888-413-8970 to get a quote. Your standard auto insurance coverage policy assists pay for repairs and replacement based upon the real cash worth (ACV) of your cars and truck. That's the quantity the car is worth on the current market, which decreases or depreciates, as it ages. This is where space insurance coverage can assist you. Prior to you purchase space insurance coverage, you must learn just how much you still owe on your vehicle loan. You can then compare it to how much your car is worth. This will help you choose if you need gap insurance or not. The Insurance Details Institute also recommends gap insurance if you:3 Put less than a 20% deposit on your vehicle Strategy to finance for 60 months or longer Bought an automobile that depreciates faster than others Have currently rolled over unfavorable equity from another vehicle loan Lease your vehicle, which usually requires gap protection To approximate your cars and truck's worth, you need to search for the Kelley Directory or National Vehicle Dealers Association value on your car. This method, you can discover out if it's best for you. Some insurance companies, like Geico, do not offer gap insurance timeshare relief company coverage, while others vary in how they use this security and how it works. How much is health insurance. Here's a glimpse at a couple of choices: The biggest auto insurance company in the United States, State Farm doesn't offer gap insurance however has actually a feature called Reward Protector, which anyone getting a vehicle loan from a State Farm bank (an alliance with US Bank) is eligible for. State Farm gap insurance coverage just looks for full protection automobile insurance coverage, but this policy doesn't always have to be underwritten by State Farm. As one of the finest automobile insurance provider, State Farm makes it easy for brand-new and existing clients to include additional functions to their policies. The Allstate space program waives the distinction between a primary auto insurance settlement and the impressive balance owed on a lorry. It waives covered losses up to $50,000 and repays a deductible payment. The deductible is the quantity you should pay prior to the insurance coverage pays the claim. Progressive caps protection at 25% of the vehicle's actual money value. You can receive space insurance protection bundled into your existing policy with the business for as low as $5 monthly. AAA provides space coverage for vehicles that are completely covered with detailed and collision insurance coverage. The insurer will waive as much as $1,000 of your deductible if your cars and truck is declared an overall loss. Esurance (and some other auto insurance provider) describes gap insurance coverage as car loan and lease protection. You'll get approved for protection if you're leasing or settling a financed vehicle and have full-coverage insurance. USAA insurance coverage is available to military and military relative. USAA uses Overall Loss Defense for automobiles more recent than 7 years of ages that have an auto loan of more than $5,000. It reimburses up to $1,000 of a deductible.

Therefore, if you didn't put much money down and you still owe a substantial amount on your total lease payment, you'll likely owe more than the car deserves if you enter a mishap. It's a good concept to compare what you'll spend for your vehicle over the life of your financing to the car's MSRP or agreed-upon list prices and see if you have a gap from the start. In case you do, space insurance is a good idea (What is collision insurance). Keep in mind your "space cost" is always fluctuating. Normally, the distinction in between what you owe and what the automobile's worth diminishes as you make month-to-month payments and as the cars and truck depreciates. The 2-Minute Rule for How Much Does Car Insurance Cost

If the preliminary loan term was short, state three years or less. Remember to cancel the protection once the amount owed on the car is less than its value. If you're unsure of whether space insurance coverage is worth it, think about the expense. Space insurance coverage is fairly inexpensive and in a lot of cases can be contributed to your existing full-coverage policy for less than $50 per year. That's most likely far less than the deficiency in between your cars and truck's value and what you owe in case of a major mishap. Like any vehicle or SUV, rented automobiles Article source depreciate quickly. For that reason, if you didn't put much money down and you still owe a sizable amount on your total lease payment, you'll cancel company likely owe more than the car is worth if you enter into a mishap.

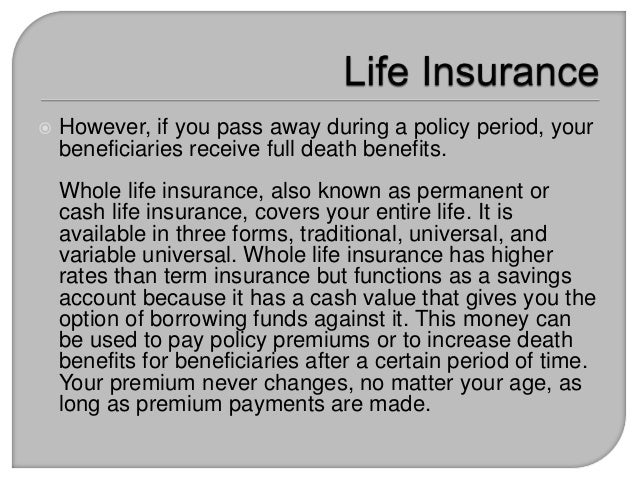

Just like a purchased vehicle, it's clever to compare your overall expense including taxes and anything else you rolled into the lease to the automobile's MSRP to figure out if you have a space. What is title insurance. If so, consider gap insurance coverage. And simply like a purchased cars and truck, the difference in between what you owe and what the vehicle's worth shrinks as you make regular monthly payments and as the automobile diminishes. So, you might not need the coverage for your whole lease duration. You might only need it for a couple of months, depending on how great of an offer you worked out. You have 3 alternatives for where to buy space insurance coverage: through the car dealership, a vehicle insurer or an insurance business. Other types are: With this type your premiums increases every year, although you pick a period of insurability that guarantees you will not need to reapply. How does cobra insurance work. It might be great for people who wish to close a short space in life insurance coverage, however a short level-term policy is likely a much better option. Here your premiums remain the same over the length of the policy however the death benefit reduces progressively over time. Home loan life insurance coverage is a kind of reducing term life. The payment is tied to the declining balance of the home mortgage, and the recipient is the home mortgage loan provider, not your household. This policy type guarantees to reimburse the premiums you paid in if you outlast the policy. As you can picture, the refund function makes the policy more costly. Return of premium term life is readily available from companies such as AAA Life Insurance, State Farm Life and Vantis Life. Make sure the policy is convertible to long-term life insurance later on. This provides you options in the future if you choose you require irreversible life insurance coverage. The policy will describe the time duration during which Informative post conversion is readily available and the kind of long-term policy offered through conversion. Ensure the policy offers sped up survivor benefit.

This, too, provides you alternatives in the future. If you have life insurance needs of various lengths, you can ladder life insurance coverage policies to conserve cash. For instance, you may buy a 30-year policy to cover the length of a home loan and a 20-year policy (or rider on the 30-year policy) to cover the time up until children are out of college. In this manner you're not grouping all responsibilities into one long policy. You often have the alternative to consist of a look for the first premium payment with your application and lock in protection from your application date forward. It's typical for an application to take a month or more to process. Ask your representative about this "short-term protection" prior to you send the application. The main kinds of life insurance are term life, entire life and universal life. And within each of those types are additional ranges. With numerous life insurance coverage options, you can likely discover a policy that fits your life insurance goals. The range of choices can seem overwhelming initially, however keeping a concentrate on the factors you require life insurance will assist you determine the ideal type. Can you define the amount and end of the financial obligation you wish to cover? For instance, this could be the quantity you anticipate to make till the year you plan to retire. Policy Kinds: ICC18-33 (10 ), ICC18-33 (15 ), ICC18-34 (20 ), ICC18-35 (30 ), L-33 (10 )( ND), L-33 (15 )( ND), L-34 (20 )( ND), L-35 (30 )( ND), L-33 (10 )( SD), L-33 (15 )( SD), L-34 (20 )( SD), L-35 (30 )( SD) Rider Types: ICC18-CIR (LT), L-CIR (LT), ICC18-WP (TERM), L-WP (TERM), L-WP (SD)( TERM), ICC17-ACDB TER, L-ACDB TER. Shopping for life insurance coverage can be puzzling if you've never ever http://remingtonjcfo177.iamarrows.com/the-facts-about-what-is-hazard-insurance-uncovered investigated it or haven't purchased it previously. This can be particularly true when comparing term and entire life insurance. However while the 2 types of policies both leave benefits after you're gone, they are really various. Understanding these distinctions is important to selecting a life insurance coverage policy that's right for you and your family. Understanding the advantages and disadvantages of each will assist you make an informed option and protect what matters most. Let's look at them now. Term insurance coverage covers a fixed period of time or term and is generally considered short-term insurance coverage. Everything about How Much Is Cobra Insurance

The average span of a term life insurance coverage policy is in between 10 and 20 years, but the term can also cover someone until they reach a defined age. These policies typically pay weslend financial the survivor benefit if you pass throughout the regard to the policy. However if the policy ends prior to you pass, the insurance provider will not pay the death advantage. In other words, when you purchase term life insurance, you are just covered for the time period that you pay the premiums. If the term of the policy ends before you pass, then the policy normally expires and the insurance provider won't pay a death benefit. A convertible policy normally allows you to convert the insurance to a various strategy. To certify for term life insurance coverage, you may have to take a medical examination. Medical tests are often needed due to the fact that the protection amounts are high. Because term life insurance coverage is uncomplicated and doesn't collect cash worth, the premiums are relatively low (depending on your age and total health) compared to entire life insurance coverage. The reason you can find lower premiums for term life insurance policies is that the coverage is just helpful for a particular amount of time (What is title insurance). But term life insurance coverage premiums depend upon a number of elements. gov tool to see if you are qualified for lower expenses. Every state has a Medicaid program and Kid's Health Insurance helping timeshare owners coverage Plan (CHIP) to supply health protection to low income people and families. How much is homeowners insurance. Contact your state Department of Insurance or Health Department to read more about these programs and if you are eligible to register. You might be eligible for Medicare if you are age 65 or oldereven if you are still workingor any age and disabled. The basic regular monthly premium for Medicare Part B (medical insurance coverage) is $144. 60 for 2020. Many people who have actually worked at least ten years and paid Medicare taxes do not pay a Part A (medical facility insurance) premium. The premium is low for high-deductible strategies and lots of strategies spend for some preventive care. The HSAs are savings accounts that you utilize to pay for medical costs not paid by your insurance. You minimize taxes with a health savings account because the cash you put in and get is either tax-free or tax-deductible. You might have the ability to save cash by choosing a high-deductible plan that will assist pay your costs if you are seriously ill or injured and an extra insurance coverage strategy. Supplemental insurance coverage provides protection for specific health conditions, such as mishaps, types of vital care, impairment, or death.

e, Health is here to help you. We have accredited insurance coverage brokers who understand the various coverage choices and can guide you through your private insurance coverage health insurance coverage choices. Our service is fast and practical and totally free of charge. Call us at (855) 396-2521 (TTY 711), Mon, Fri, 9am7:30 pm ET, or email us at sales@ehealth. com. This post is for basic information and may not be updated after publication. Consult your own tax, accounting or legal consultant instead of counting on this post as tax, accounting, or legal advice (What is hazard insurance). A is the charge you should spend for your health insurance policy. Premiums are generally paid monthly, quarterly, or annual during your duration of coverage. Understanding how the cost of your premium can affect the amount of protection you receive will assist you make an informed choice as you look for a strategy for your household. Instead of search for medical insurance on your own, contact Health, Markets. Because 2010, we have actually helped Americans enlist in the best health care strategies from our varied portfolio of items. Our local, certified agents are readily available at your benefit to walk you through your alternatives. Contact us today to discover how you can get cost effective healthcare. Continue reading for more information about the ins and outs of medical insurance premiums. It is essential to comprehend how premiums differ from other out-of-pocket healthcare costs you might experience. In addition to paying your premium, you may also be accountable for particular expenses and services you get through your strategy. Your, or copay, "is a set amount that you pay in addition to your premium for covered healthcare services including doctor's visits, professional sees, or prescription drugs. As soon as your copay is paid, your medical insurance service provider covers the remaining expense of the service. For instance, presume you have to go in for a covered procedure that costs $3,000. Your deductible is $1,000. In this scenario, your strategy will not pay anything up until you have actually met your $1,000 deductible for this covered procedure. The deductible might not use to all services." With, Discover more "you and your health insurance coverage business each pay for a percentage of your health insurance coverage expenses when you satisfy your deductible. A typical example is an 80/20 coinsurance strategy. For instance, let's state your health insurance strategy's enabled amount for a workplace visit is $100 and you've fulfilled your deductible. Your coinsurance quantity of 20% would be $20 and the medical insurance plan pays the rest of the permitted quantity. Even if 2 individuals are enrolled in the very same health insurance, they might still pay different premiums rates. Your health and lifestyle can be factored into the amount you spend for health insurance coverage. The aspects that can impact your premium rates consist of: Those who currently utilize cigarettes, chewing tobacco, or snuff can risk being charged a high premium rate. You may even have to pay a greater premium if you have actually recently given up using tobacco. This is due to the risk of cancer and illnesses that result from regular usage of tobacco products. Typically the more youthful you are, the lower your premium. The Definitive Guide for What Is The Best Dental Insurance

Depending on whether you're buying health insurance for yourself or for your spouse and/or children, you might be charged a greater premium the more individuals are included to your plan. Each plan classification, or metal level, is designed to pay a different percentage of you health care costs. Normally, the greater the metal level, the greater the premium. What is liability insurance. For elements including climate or a lack of healthy food choices, Americans who reside in the very same location might have the very same health dangers as each other. Since of this, health insurance companies consider where you live when identifying your premium. Insurance suppliers might also just be available in specific areas, so lower-premium choices may not be offered and prices may be higher. There are four levels of protection that Americans might register in: You can pay the lowest quantity in premiums to receive an approximated 60% protection from your health insurance coverage service provider for your healthcare services. This will leave you to pay 40% out of pocket. You can pay a lower amount in premiums to get an estimated 70% coverage from your health insurance coverage supplier for your healthcare services. This will leave you to pay 30% expense. You can pay a greater amount in premiums to get an approximated 80% coverage from your health insurance service provider for your healthcare services. You can pay the greatest amount in premiums to get an estimated 90% protection from your health insurance supplier for your health care services. This will leave you to pay 10% expense. There are also that mainly advantage healthy individuals under the age of 30 who want coverage in case of a major, unforeseen medical issue. These plans have the most affordable premiums availableeven lower than a Bronze plan. However this low premium comes at a risk. You could be facing a deductible higher than $6,000 for an individual. With the ACA, those with a disastrous strategy can still receive the exact same covered preventive care services and important health advantages as those who enlist in a metal level plan.

If you are worried about your ability to pay your premiums, you might receive subsidies from the federal government. The is a subsidy that assists lower or cover the cost of premiums for families making a modest earnings. You can get this credit in one of 2 ways: You can have the credit paid directly to your medical insurance company to lower or cover the cost of your premiums. You can claim all the credit you are qualified to get when you submit your yearly tax return. To be eligible for the premium tax credit, you must satisfy these requirements: Your yearly family earnings need to be between 100% and 400% of the Federal Poverty Line. I have actually skipped it lots of times, and my number has yet to come up. If it turns out that I require to cancel or disrupt, I'll simply have to take my monetary swellings I played the chances and lost. However sometimes it's probably an excellent concept to get this coverage for example, if you're paying a lot of up-front money for an arranged trip or short-term accommodation leasing (both of which are pricey to cancel), if you or your travel partner have questionable health, or if you have an enjoyed one in the house in bad health. A basic trip-cancellation or disruption insurance plan covers the nonrefundable financial charges or losses you sustain when you cancel a prepaid tour or flight for an acceptable reason, such as: You, your travel partner, or a relative can not travel since of sickness, death, or layoff, Your trip business or airline fails or can't perform as guaranteed A member of the family in the house gets ill (check the fine print to see how a household member's pre-existing condition may impact coverage) You miss a flight or require an emergency flight for a factor outside your control (such as a cars and truck accident, harsh weather, or a strike) So, if you or your travel partner inadvertently breaks a leg a few days before your journey, you can both bail out (if you both have this insurance coverage) without losing all the cash you spent for the journey. This kind of insurance can be utilized whether you're on an organized tour or cruise, or traveling separately (in which case, only the prepaid expenses such as your flight and any nonrefundable hotel appointments are covered). Note the distinction: Trip cancellation is when you do not go on your journey at all. Journey interruption is when you start a journey but have to suffice short; in this case, you'll be reimbursed just for the portion of the trip that you didn't total. If you're taking a tour, it may currently include some cancellation insurance ask - What is hazard insurance. Some insurance providers will not cover particular airline companies or tour operators. Ensure your provider is covered. Purchase your insurance plan within a week of the date you make the very first payment on your trip. Policies purchased behind a designated cutoff date generally 7 to 21 days, as figured out by the insurance provider are less most likely to cover tour company or air provider insolvencies, pre-existing medical conditions (yours or those of member of the family at house), or terrorist events. Mental-health concerns are typically not covered. Tense tourists are complaining about two huge unknowns: terrorist attacks and natural disasters. Ask your company for details. A terrorist attack or natural disaster in your home town may or may not be covered.

Even then, if your tour operator uses a substitute schedule, your protection may become space. As for natural catastrophes, you're covered only if your destination is uninhabitable (for example, your hotel is flooded or the airport is gone). War or outbreaks of disease generally aren't covered. With travel turned upside down by the coronavirus pandemic, it's more vital than ever to understand what travel insurance covers and what it doesn't. While many standard policies offer protection for flight cancellations and journey disruptions due to unpredicted occasions, the majority of COVID-19related issues are excluded from protection, consisting of: Fear of travel: If you choose not to take a trip out of fear of contracting COVID-19, your insurance plan won't cover you. Getting My What Is Deductible In Health Insurance To Work

Additional COVID-19 break outs: If the location you're preparing to go to experiences brand-new shutdowns after you have actually scheduled the trip, do not seek to your travel insurance coverage for protection. Going versus government travel warnings: If you do have coverage, your policy may be voided if you take a trip somewhere that your government has actually deemed hazardous, or if your federal government has restricted worldwide travel. You might have the ability to prevent the concern of what is and what isn't covered by buying an expensive "cancel for any factor" policy (explained listed below). Health emergency situations are the main cause for trip cancellations and disruptions, and they can include high medical expenses as well as extended lodging bills for travel partners. While lots of US insurance providers cover you overseas, Medicare does not. Also, be sure you know any policy exclusions such as preauthorization requirements. Even if your health insurance does cover you globally, you may desire to consider buying an unique medical travel policy. Much of the additional protection offered is additional (or "secondary"), so it covers whatever expenditures your health strategy doesn't, such as deductibles. However you can likewise purchase main protection, which will look after your expenses up to a specific amount. In emergency situations involving expensive treatments or over night stays, the hospital will generally work straight with your travel-insurance provider on billing (however not with your regular health insurance company; you'll likely need to pay up front to the health center or center, then get compensated by your stateside insurance company later on). Whatever the scenarios, it's smart to contact your insurance provider from the road to let them know that you have actually looked for medical help. Lots of pre-existing conditions are covered by medical and trip-cancellation protection, depending on when you purchase the coverage and how just recently you have actually been dealt with for the condition. If you travel often to Europe, multi-trip annual policies can conserve you cash. Talk to your agent or insurance provider before you dedicate. The United States State Department occasionally concerns warnings about taking a trip to at-risk nations. If you're visiting one of these countries, your cancellation and medical insurance will likely not be honored, unless you buy additional coverage. Compare the expense of a stand-alone travel medical strategy with thorough insurance coverage, which comes with great medical and evacuation protection. A travel-insurance company can assist you figure out the choices. Specific Medigap plans cover some emergency care outside the US; call the company of your supplemental policy for the information. Theft is especially uneasy when you consider the dollar worth of the products we pack along. Laptops, tablets, electronic cameras, smart devices, and e-book readers are all pricey to change. One method to protect your financial investment is to buy travel insurance coverage from a specialized business such as Travel Guard, which uses a variety of options that include coverage for theft. What Is A Deductible Health Insurance Can Be Fun For Anyone

It's likewise clever to consult your property owners or renters insurance provider. Under most policies, your personal effects is currently protected versus theft throughout the world but your insurance deductible still applies. If you have a $1,000 deductible and your $700 tablet is taken, you'll need to pay to change it. Instead of buying different insurance, it might make more sense to add a rider to your existing policy to cover costly items while you travel. Before you leave, it's a good concept to take a stock of all the high-value products you're bringing. Make a list of identification numbers, makes, and designs of your electronic devices, and take pictures that can function as records. If you have lorries you utilize for your service operation or are owned by the business, you will require a commercial car insurance plan. This policy covers your liability associated with the operation of the vehicle and any damage triggered to the lorry. More helpful hints If your business owns automobiles, this industrial car liability is required by state law. At Landes, Blosch, we recommend car liability limits of a minimum of $1,000,000 to protect the company. If your cars are bigger than pickup, we often recommend an excess policy to increase the auto limits. If you own a business, you have or might have staff members whom you are accountable for.

These medical expenses can get very costly, depending upon the intensity of the mishap. This coverage takes care of both the medical expenses and payments to the employee for the time they are not able to work. In a lot of states, this coverage is required if you have employees who aren't household members or owners in the business. In the majority of states, you acquire this policy through private insurance coverage carriers. Although, in North Dakota, Ohio, Washington, Wyoming, Puerto Rico, and the U.S - What is liability insurance. Virgin Islands, you acquire employees' settlement through the state fund. Commercial insurer need a basic way to understand various organization threats and the scale of an insuree's operations. As always in the insurance market, there are many different approaches and circumstances to accomplish the very same thing, however here are 2 primary ways business insurance coverage ratings work. Insurer require to understand the liability risk of a company since they will be spending for the associated liability judgments. Typically, insurance coverage business will take the loss data from thousands of business comparable to yours and establish a rate that will permit a pool of consumers with comparable operations to spend for each others' losses. The majority of the time, this ranking figure is based on the revenue of your company increased by the loss rate of the danger pool. For business such as construction, the rate will be based upon payroll rather of revenue. No matter your service type, discover out what your liability premium is based on and ensure http://andyodaw726.timeforchangecounselling.com/what-is-group-term-life-insurance-fundamentals-explained to keep that figure upgraded throughout the year to avoid an audit. Although similar to liability coverage, property protection can be a little more complicated to cost. There are lots of various kinds of property and methods to price them. Most typically, the figures are rated on the industry type that occupies the building or owns the contents, because that is how the residential or commercial property will be made use of. The 2nd ranking element is based upon the building of the building.

For example, a wooden-frame building will have a greater danger for fire than a metal building (specifically if the wooden-frame building does not have a sprinkler system). Lastly, one of the most important, if not the most important rating factor, is the location of your property. This will identify your direct exposure to catastrophic loss such as cyclones, wildfires, tornadoes, earthquakes, and floods. Insurance coverage underwriters will condense all these variables into a mark dickey salesforce regional property rate that is the total insured worth increased by the residential or commercial property direct exposure rate. Safeguarding your financial investment in your company is a vital part of developing a company that lasts. A Biased View of How Much Is Boat Insurance

There are numerous elements to think about when opening your own business, consisting of the importance of having Home insurance. It covers the repair work and replacement of specific business properties ought to a covered occurrence like fire, theft or vandalism occur. It's an especially important coverage since many small companies and start-ups do not have the money to replace what's needed to keep a service running. Home insurance assists cover the damage or loss of your home, like structures or structures, and items including equipment, furnishings, inventory, supplies and fixtures. It can likewise help cover the expenses to repair or change taken, damaged or damaged home, consisting of home and equipment that isn't yours but remains in your care and custody. Your insurance coverage representative can help you customize your protection to deal with the particular dangers facing your organization, including selecting the type of Home insurance protection you might require. There are generally 2 kinds of coverage used by insurer: replacement expense or real cash value. Replacement Expense: Pays to repair or reconstruct home with products of the exact same or similar quality. Actual Cash Value: Pays the existing worth of the harmed property, the cost to reconstruct or change home, generally replacement minus depreciation. In lots of cases, business owners lease space to run their operations. If you fall under this classification, inspect your lease to evaluate your responsibilities in regards to insurance. It's a good concept to evaluate the lease with your insurance representative to verify the insurance coverage you choose suffices and will secure you in the occasion of damage or loss of the residential or commercial property. There are numerous factors that enter into figuring out the expense of your service home insurance coverage, consisting of: The value of the residential or commercial property being covered, The place of your company, and The protection limitations and deductible you pick. It is necessary to comprehend that a residential or commercial property insurance coverage does not cover all legal threats to your company. Typically speaking, any automobiles based on motor vehicle registration; money or securities; land, water and living plants; and outdoor fences or signs not connected to the building might not be covered by your home insurance plan - What does renters insurance cover. Talk to a certified agent about what is and is not covered by your residential or commercial property insurance coverage and any protections you need to think about acquiring to assist protect your organization. To find out more about Home insurance and other company insurance services, contact a Travelers independent representative. Here are some of the more crucial terms to assist you understand your policy. Does your company have workers? You may be needed to have employees comp insurance coverage. See how this coverage safeguards you and your staff members. General liability can assist you protect your company if someone claims that it triggered them harm or loss and they take legal action. Discover items by market: Customize your Service Get the personal service and attention that a representative provides. Discover a local representative in your area:. The 9-Second Trick For How Much Is Boat Insurance

Share this on: For the a lot of part, industrial health insurance coverage is specified as a medical insurance strategy not administered by the federal government. How much does car insurance cost. (Medicare Benefit, which is a federal government strategy, is administered by personal insurance companies authorized by Medicare). You may get industrial insurance through your company or your partner's employer, or as part of your household's plan if you meet particular requirements. Nearly half of Americans receive business insurance coverage through their job, according to information from the Kaiser Family Foundation. You can likewise purchase health insurance straight from an insurance carrier, through the federal market, or through an insurance coverage broker. Business insurance coverage plans are available in 2 varieties: specific or group. For more help, check in with your agent. They're the very best resource to help you figure out how much life insurance protection is right for you. The expense of entire life insurance is frequently overestimated, and Find more info it may be more economical than you believe. The following are some elements that play a huge function in determining your whole life insurance coverage premium: Your age Your gender Your health Protection quantity Generally, the younger and much healthier you are, the lower your entire life insurance coverage rate will be. To discover more, talk to your agent about what the cost of whole life insurance coverage would be for you. Some policies have the option to convert term life insurance coverage to entire life protection. A convertible insurance plan, like American Household Life Insurance provider's Dream, Secure Term Life Insurance coverage, enables you to transform a portion or all of your existing term life insurance coverage policy during the conversion eligibility duration. You can do this without needing to take a medical exam or go through other screening that could affect your eligibility. This conversion choice provides the benefit of starting with a less expensive term life insurance coverage policy (compared to a whole life policy, for instance), while still being able to convert to a long-term policy later on if your insurance coverage needs and financial methods alter.

American Domesticity Insurer offers a variety of extra coverages that you can acquire to develop a whole life insurance policy that matches your requirements. Here are some of the additional coverages offered: Enables the purchase of extra irreversible life insurance without medical concerns or an examination at defined dates and life events. ** Offers $15,000 of protection on natural, embraced and stepchildren. Waives premiums if the insured becomes completely disabled. In addition to the protections offered for purchase pointed out above, each policy immediately features an Accelerated Death Benefit choice (to be added sometimes of requirement). This advantage enables the policy owner to gather a part of the death benefit under specific conditions if the primary insured is diagnosed with a terminal health problem. *** Are you ready to take the next action in assisting to prepare for your family's financial future and buy whole life insurance coverage? Contact an American Family Insurance coverage representative to read more about personalized life insurance protection that assists you safeguard what matters most. Repaired and ensured premiums are declarations about the policy as identified at issue, and any made to a policy may impact the premium and are subject to our underwriting rules. The words life time, lifelong and long-term go through policy terms and conditions. This policy grows at age 121. Please contact an American Household representative for information on protections and constraints. * Any loans drawn from your life insurance policy will accumulate interest. Any exceptional loan balance (loan plus interest) will be deducted from the death benefit at the time of claim or from the money worth at the time of surrender. ** The Surefire Purchase Alternative might be exercised only at specified dates and life events and undergoes Have a peek at this website benefit amount limitations. See rider for extra details. *** Working Out the Accelerated Death Benefit alternative might have tax effects and could impact credentials for government advantages. Policy Kinds: ICC18-33 (10 ), ICC18-33 (15 ), ICC18-34 (20 ), ICC18-35 (30 ), L-33 (10 )( ND), L-33 (15 )( ND), L-34 (20 )( ND), L-35 (30 )( ND), L-33 (10 )( SD), L-33 (15 )( SD), L-34 (20 )( SD), L-35 (30 )( SD), ICC18-36 (10 ), ICC18-36 (15 ), ICC18-36 (20 ), ICC18-36 (30 ), L-36 (10 )( ND), L-36 (15 )( ND), L-36 (20 )( ND), L-36 (30 )( ND), L-36 (10 )( SD), L-36 (15 )( SD), L-36 (20 )( SD), L-36 (30 )( SD), ICC17-225 WL, L-225 (ND) WL, L-225 WL, ICC17-226 WL, L-226 (ND) WL, L-226 WL, ICC17-227 WL, L-227 (ND) WL, L-227 WL, ICC19-97 UL, L-97 UL (ND), L-97 UL) Rider Forms: ICC17- GPO WL, L-GPO WL, ICC17-CIR WL, L-CIR WL, ICC17-WP WL, L-WP WL, L-WP (SD) WL, ICC17-ACDB WL, L-ACDB WL. Getting My How Long Do You Have Health Insurance After Leaving A Job? To Work

Each time you make an exceptional payment toward your long-term policy, a portion of that payment covers the expense of your insurance and policy charges and the remainder is used to fund your cash worth account. From the first day, any cash worth that collects grows tax-deferredas long as the policy is in force. The development prospective varies among the different types of irreversible policies depending upon what type of interest is credited and, for Variable Universal Life policies, the performance of the underlying investment choices picked. The cash in the money value account can be a flexible resource to assist you reach monetary goals. How much is homeowners insurance. You want to secure your family. You know you need some type of life insurance coverage. However what type of policy should you purchase? The decision appears more difficult than it requires to be. That's why we desire to describe your choices so you can make the protection choice that's right for you and your family. You most likely have experienced a number of different types of life insurance coverage in your search for peace of mind term life, whole life, universal life, guaranteed issue, unintentional death The list goes on. The bright side is, there are just 2 types of life insurance that you actually need to comprehend: Term and irreversible. The best kind of life insurance coverage for you will depend on your budget plan and how long you want coverage. Entire life insurance coverage policies can cost anywhere from 5 to 20 times more than a term life insurance coverage policy because they cover insurance policy holders over their whole lives, unlike term life insurance coverage, which has a set duration of coverage. The expense of protection may have you asking: Is whole life insurance coverage deserves it? Excellent concern. It is necessary Click here for info to comprehend the differences between whole life insurance coverage and term life insurance coverage to discover the answer that works finest for your enjoyed ones. Entire life insurance coverage is a type of permanent life insurance coverage policy that lasts as long as you keep paying your premiums. Generally, the death advantage on an entire life policy is ensured to go to your recipients, no matter just how much time has actually expired since you bought a policy. How to become an insurance agent. For instance, if you buy an entire life insurance coverage policy when you are 20, your life insurance business will pay a survivor benefit to whoever is named as your recipient, no matter when you pass away even if you live to be more than 100 years of ages. Simply like with any type of life insurance coverage, the younger and much healthier you are when you purchase a policy, the more economical the policy will be. Whole life insurance coverage consists of a cash accumulation part referred to as the policy's cash worth that can grow in time. The money worth grows over time and the gains are tax-deferred, which implies you will not pay taxes on the gains while they grow. Some entire life insurance policies are likewise qualified to get dividends. These dividends represent a part of the life insurance business's revenues. While the death advantage of an entire life insurance coverage policy can secure your family financially if you were to die (by assisting to replace your earnings, for example), the money value of an entire life policy builds up as premiums are paid. |

RSS Feed

RSS Feed